ITIN Mortgages in Florida: Requirements, Best-Fit Borrowers, and Common Documentation Problems

If you’re shopping for a mortgage in Florida with an ITIN instead of a Social Security Number, you are not playing in the standard Fannie/Freddie/FHA sandbox. You’re in Non-QM / specialty lending, where the rules are lender-made, pricing is higher, and documentation mistakes kill deals fast. Here’s what actually works—and where ITIN borrowers blow themselves […]

BRRRR in Miami: Financing Timeline, Seasoning Rules, and How to Avoid the “Stuck Refi” Trap

BRRRR works beautifully on paper. In Miami, it blows up more often—because investors don’t understand seasoning requirements, appraisal reality, insurance volatility, or lender timelines. BRRRR isn’t about buying cheap. It’s about exiting the first loan cleanly and predictably. Here is the real Miami playbook—minus the fantasy math. 1) The BRRRR Financing Timeline (Reality, Not Instagram) […]

Citizens Insurance + Mortgages: What Buyers Need to Know Before They Go Under Contract

If you’re counting on Citizens Property Insurance to make the deal work, you need to treat insurance like a loan condition, not an afterthought. In Miami, insurance is one of the most common reasons closings get delayed or budgets blow up—because the lender won’t fund without proof of acceptable coverage. 1) Citizens isn’t “just another […]

Buying Miami Investment Property in an LLC: What Changes (Rates, DP, Reserves, Liability)

Buying an investment property in Miami through an LLC can be smart—but most investors do it for the wrong reasons and then get shocked by the financing terms. The lender doesn’t care about your “asset protection story.” They care about risk, recourse, and exit liquidity. An LLC increases perceived risk, so underwriting usually tightens. Here’s […]

Refinancing a Rental Property in Florida: DSCR vs Conventional vs Portfolio—When Each Wins

Refinancing a Florida rental isn’t about finding “the lowest rate.” It’s about choosing the loan type that fits your income documentation, property cash flow, and exit plan. The wrong choice wastes months, triggers underwriting chaos, or boxes you into bad terms. Here’s how DSCR, conventional, and portfolio refis compare—and when each one is the smart […]

DSCR Loans for Short-Term Rentals in Florida: What Lenders Really Use for Income

DSCR loans for short-term rentals (STRs) aren’t underwritten like your normal mortgage. The lender usually doesn’t care what you earn from your job. They care whether the property’s income can cover the mortgage payment—and for STRs, the fight is always the same: What income counts, and how do you prove it without turning your closing […]

Construction-to-Permanent Loans in Miami: Build, Pay, and Convert Without Two Closings

A construction-to-permanent loan (often called a “one-time close”) is designed for buyers who want to finance the land (or lot) + construction costs now, then automatically convert into a long-term mortgage when the home is finished—without doing a second closing. It’s powerful. It’s also one of the easiest loans to derail in Miami if you […]

Jumbo Loan Underwriting in Miami: Reserves, Assets, and What Triggers Extra Scrutiny

Jumbo loans are portfolio loans (not sold the same way conforming loans are), so underwriting is stricter for one reason: the lender is taking more concentrated risk. In Miami, that risk gets amplified by condos, insurance volatility, and large asset movements. Here’s what underwriters focus on, what “reserves” really mean, and the exact issues that […]

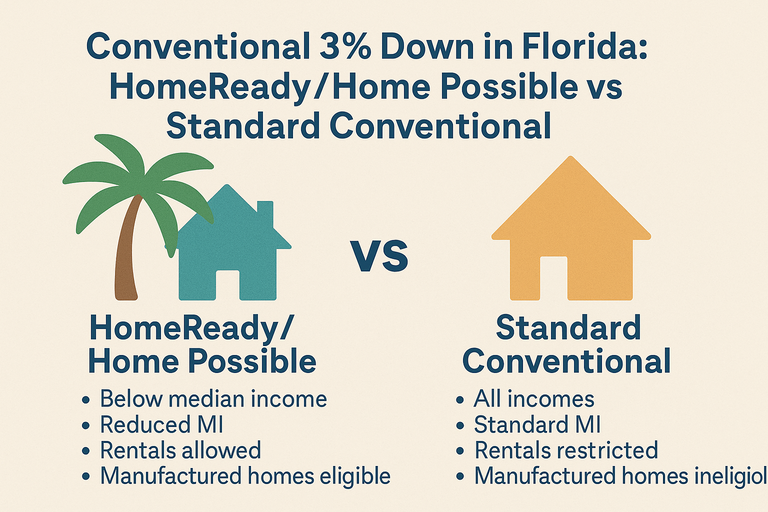

Conventional 3% Down in Florida: HomeReady/Home Possible vs Standard Conventional

If you’re shopping “3% down” in Florida, you’re really choosing between two buckets: Affordable-lending conventional (HomeReady / Home Possible) Standard conventional at 97% LTV (often called “Conventional 97”) They can look identical on a pre-approval letter. Underwriting doesn’t treat them the same. The quick difference (what most buyers miss) HomeReady (Fannie Mae) / Home Possible […]

VA Loans in Miami: Residual Income, Condo Rules, and the Truth About “Zero Down” Costs

VA loans are one of the best benefits in housing—but Miami is where sloppy assumptions get expensive. The three places buyers get blindsided are residual income, condo approval, and thinking “zero down” means “no money needed.” 1) Residual income: VA’s real affordability test Most loan programs obsess over DTI. VA cares about how many dollars […]

FHA Condo Loans in Miami: Approval Lists, Spot Approvals, and Common Denial Reasons

FHA can be a great path for Miami condo buyers—but only if the condo project (or your single unit) meets FHA rules. The #1 mistake is going under contract first and “hoping it’s FHA-approved.” That’s how timelines blow up. 1) How to check if a Miami condo is FHA-approved (the official list) HUD maintains the […]

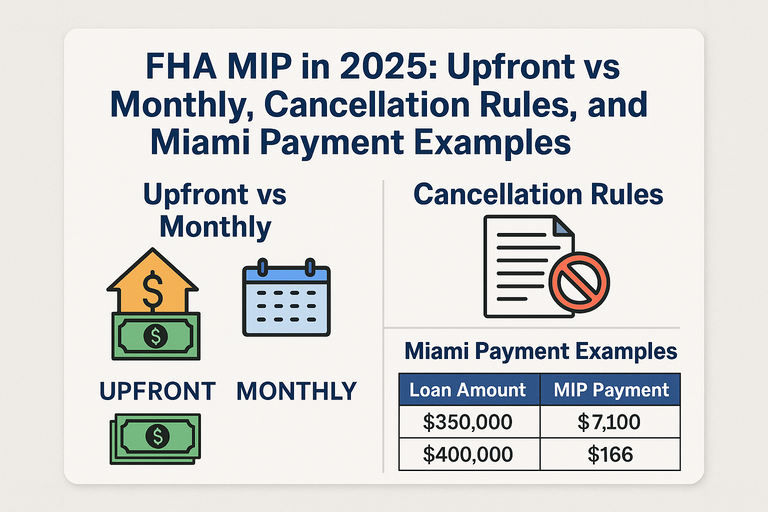

FHA MIP in 2025: Upfront vs Monthly, Cancellation Rules, and Miami Payment Examples

FHA mortgage insurance (MIP) has two separate charges: an upfront fee at closing and an annual fee paid monthly. People mix these up—and that leads to bad payment expectations. 1) Upfront MIP (UFMIP): the one-time charge For most FHA forward loans, the Upfront MIP is 1.75% of the base loan amount. How it’s paid: You […]

Florida Down Payment Assistance Programs (2025–2026): Who Qualifies and How to Apply

Down payment assistance (DPA) in Florida is real—but it’s not “free money.” Most programs are second mortgages (deferred, forgivable, or low-payment) with strict rules, income limits, and paperwork. If you wait until after you’re under contract to figure it out, you’re asking for delays. Below are the programs Miami-area buyers most commonly use in 2025–2026, […]

Property Taxes After Purchase in Miami-Dade: Why Your Escrow Payment Jumps (and how to plan)

If you buy a home in Miami-Dade and assume the property taxes will stay close to what the seller paid, you’re setting yourself up for an ugly surprise. Miami-Dade’s Property Appraiser warns buyers directly: a change in ownership may reset assessed value to full market value, which can raise taxes. That reset is the #1 […]

Miami Appraisal Gaps: What To Do When the Appraisal Comes in Low

A low appraisal in Miami is common when prices move faster than comparable sales, when a property is unique, or when buyers overbid in competitive neighborhoods. The lender doesn’t care what you offered. They lend based on appraised value. If the appraisal comes in low, you have an “appraisal gap” and you have to solve […]

Hurricane Season Closings: Insurance Binders, Moratoriums, and How to Avoid Delays

Hurricane season in South Florida doesn’t just threaten the weather—it threatens your closing timeline. The #1 failure point isn’t the lender. It’s insurance binding. If you can’t produce an acceptable insurance binder on time, many lenders won’t fund. Here’s what buyers need to know before they go under contract in Miami-Dade. What an insurance binder […]

Unwarrantable Condos in Miami: What It Means and How You Can Still Get Financing

In Miami, a condo can be “perfect” and still be unwarrantable—meaning it doesn’t meet Fannie Mae/Freddie Mac condo project eligibility for standard conventional financing. That doesn’t automatically kill the deal. It just changes your financing path, your down payment, and your timeline. Here’s what makes a condo unwarrantable, how to find out early, and what […]

Mortgage Rate Lock in Miami (2025–2026): When to Lock, Float, or Renegotiate

If you’re buying in Miami, a rate lock isn’t a “nice-to-have.” It’s a risk management decision that can save (or cost) you thousands. Most buyers get this wrong by treating it like a guess about the Fed. Don’t. Treat it like protecting your budget and your closing date. Here’s how to decide when to lock, […]

Flood Zones in Miami-Dade: How FEMA Maps Affect Your Payment and Approval

In Miami-Dade, your flood zone isn’t trivia—it can change your monthly payment, your cash-to-close, and sometimes your ability to close on time. Lenders don’t “prefer” flood insurance. In many cases, they’re legally required to make sure it’s in place before funding. Here’s how FEMA maps drive the outcome and what you should do before you […]

Wind Mitigation Reports: How They Reduce Insurance (and Improve Mortgage Approval Odds)

In Miami, a wind mitigation report isn’t “nice paperwork.” It can directly lower your homeowners insurance premium and, more importantly, reduce the chance your mortgage gets delayed because insurance comes in too expensive or too slow. A wind mitigation inspection documents hurricane-resistance features using Florida’s Uniform Mitigation Verification Inspection Form (OIR-B1-1802). What a wind mitigation […]