DTI (debt-to-income ratio) is the percentage of your gross monthly income that goes to monthly debt payments. Lenders use it to judge whether your payment is sustainable—especially in Miami, where HOA dues + insurance can blow up the “housing payment” number.

DTI formula:

DTI = (monthly housing payment + monthly debts) ÷ gross monthly income

Monthly housing payment usually includes: principal + interest + property taxes + homeowners insurance + HOA/condo fees (and often flood insurance if required).

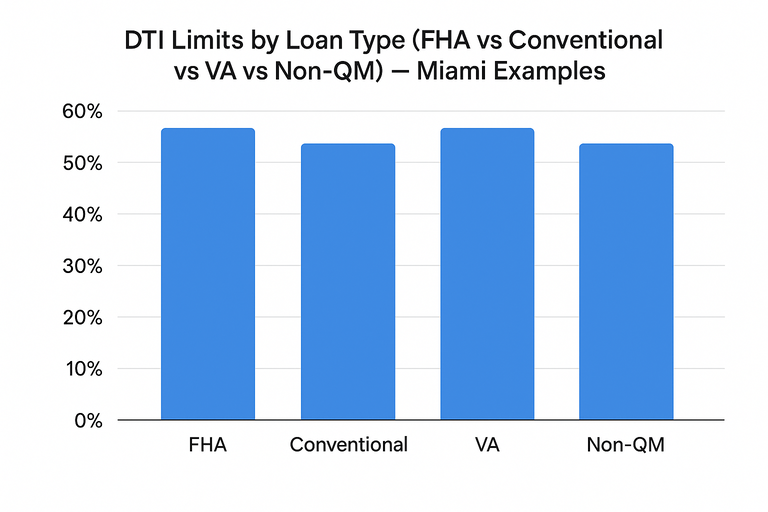

Conventional (Fannie Mae / Freddie Mac): commonly up to 50% with AUS

For many conventional loans run through automated underwriting (DU), DTI can go up to 50% depending on the overall risk profile.

That doesn’t mean 50% is “easy.” It means the AUS might approve it if the rest of the file is strong (credit, reserves, low risk layering).

Miami example (Conventional):

- Gross income: $10,000/mo

- Housing (PITI + HOA): $4,200/mo

- Other debts: $700/mo

- Total debt: $4,900/mo → DTI = 49%

This is possible in conventional—if the system likes the file and the condo/project doesn’t trigger extra risk.

What trips people up in Miami: HOA dues and condo requirements can push DTI over the line even when the mortgage amount seems fine.

FHA: manual ratios vs AUS approvals (big difference)

FHA is often described as “flexible,” but the real story is split:

- Manual underwriting is typically 31% front-end / 43% back-end (classic FHA benchmark referenced widely and consistent with FHA policy discussions).

- With automated underwriting (AUS) and strong compensating factors, many lenders can approve higher total DTIs (you’ll often see higher caps discussed in the market), but overlays vary by lender.

Miami example (FHA):

- Gross income: $7,500/mo

- Housing (PITI + HOA): $2,650/mo

- Other debts: $650/mo

- Total debt: $3,300/mo → DTI = 44%

That might be too high for strict manual limits, but could be approvable via AUS depending on the full profile.

Reality check: If your score, reserves, or documentation are weak, FHA “flexibility” disappears fast.

VA: DTI is not a hard cap, but 41% is a key pressure point

VA underwriting emphasizes residual income (money left after expenses) more than a strict DTI cap. The VA has a long-standing guideline that DTI above 41% requires closer scrutiny, and approval relies heavily on residual income and compensating factors.

Miami example (VA):

- Gross income: $9,000/mo

- Housing: $3,600/mo

- Other debts: $600/mo

- Total debt: $4,200/mo → DTI = 46.7%

This can still work on VA if residual income is strong and the file supports it.

Brutal truth: If you’re counting on VA to “ignore DTI,” you’re playing yourself. VA can be flexible, but it’s not a free-for-all.

Non-QM: lender-specific—and sometimes DTI isn’t the main metric

Non-QM is not one program. It’s a category. DTI limits vary by product and lender.

Two common Non-QM realities:

- Bank statement / alternative income programs often allow higher DTIs than strict agency guidelines, but the exact cap depends on the lender and your overall profile.

- DSCR loans for investors often don’t use personal DTI the same way—approval is driven by the property’s cash flow.

If you want to internally link the non-QM angle on your site:

- Bank statement program: https://mymiamimortgagebroker.com/bank-statement-loans-miami/

- Investor comparison: https://mymiamimortgagebroker.com/dscr-loan-vs-bank-statement-loan/

Miami-specific DTI killers (don’t ignore these)

- HOA/condo dues: They count in housing payment and can be massive.

- Insurance: Homeowners + wind + flood (when required) changes affordability.

- Property taxes: Your escrow can jump after purchase.

- Undisclosed debt: BNPL, deferred student loans, or co-signed loans can surface mid-underwriting.